- VA refinance options include the VA Streamline (IRRRL) to lower your rate with less documentation and the VA Cash-Out refinance to access home equity.

- VA refinancing often offers lower rates and fewer requirements than many conventional refinancing options.

- A VA refinance may make sense if you can secure a lower interest rate and stay in your home long enough to recoup closing costs.

Qualified Veterans and active-duty service members can refinance a VA loan. The VA home loan refinance program provides eligible homeowners with a simple way to take advantage of lower rates and decrease their monthly mortgage payment.

Beyond that, Veteran and military homeowners can get cash back on a VA refinance and use the proceeds for a variety of needs, from paying off debt or making home improvements and much more.

With VA mortgage rates remaining volatile, now could be a smart time for some military homeowners to explore refinancing with a VA loan. Even if conditions aren’t ideal today, staying informed can help you move quickly when the right opportunity arises.

As of today, July 28th, 2026, the 30-year fixed VA refinance loan rate is 5.875%, unchanged from last week's average of 5.875%. See more rates, including assumptions, in the table below.

VA Refinance Rates Today

VA loan refinancing rates change daily based on market conditions. See current VA refinance rates for each VA loan type below.

| VA Loan Type | Interest Rate | APR | Points |

|---|---|---|---|

| 30-Year VA Cash-Out Refinance | 6.375% | 6.709% | 0.3750 ($1106.25) |

| 30-Year VA Cash-Out Jumbo Refinance | 6.375% | 6.697% | 0.2500 ($1916.38) |

| 30-Year Streamline (IRRRL) Refinance | 5.875% | 6.185% | 1.8750 ($5531.25) |

| 30-Year Streamline (IRRRL) Jumbo Refinance | 6.125% | 6.382% | 1.2500 ($9581.89) |

To get started, call 1-800-884-5560 or start your VA refinance online.

Two main programs help borrowers with VA loans refinance to a lower rate: the VA Streamline refinance, also known as the Interest Rate Reduction Refinance Loan (IRRRL), and the VA Cash-Out refinance.

Two Great VA Loan Refinancing Options

| VA Streamline (IRRRL) Refinance | VA Cash-Out Refinance |

|---|---|

| Often called a "streamline" refinance, the Interest Rate Reduction Refinance Loan (IRRRL) option is designed to help current VA loan holders lower their monthly payments by refinancing to a lower interest rate with fewer steps. More on IRRRL VA Refinancing |

A "cash-out" refinance is an option for eligible homeowners with either a VA or non-VA loan looking to take advantage of their home's equity to access cash for home improvements, emergencies, pay off debt or any other purpose. More on VA Cash-Out Refinancing |

A VA Streamline refinance allows Veterans who currently have a VA loan to refinance into a lower interest rate, reducing monthly mortgage costs. Streamline refinance loans feature little paperwork and often require little to no cost out-of-pocket. Borrowers can roll closing costs into their overall loan amount, and some homeowners can also secure a streamline refinance without an appraisal.

The other popular option, known as the VA Cash-Out refinance, allows borrowers to tap into their home's equity and use it as cash. This type of refinance is available to any qualified Veteran homeowner, regardless of whether they have an FHA, USDA or conventional loan.

It’s important to treat refinancing as a strategic decision and not just a reaction to market trends.

Homeowners should understand that refinancing may result in higher finance charges over the life of the loan.

So, it's wise to crunch the numbers beforehand. Estimate your potential savings using our VA refinance calculator for streamline and cash-out refinances.

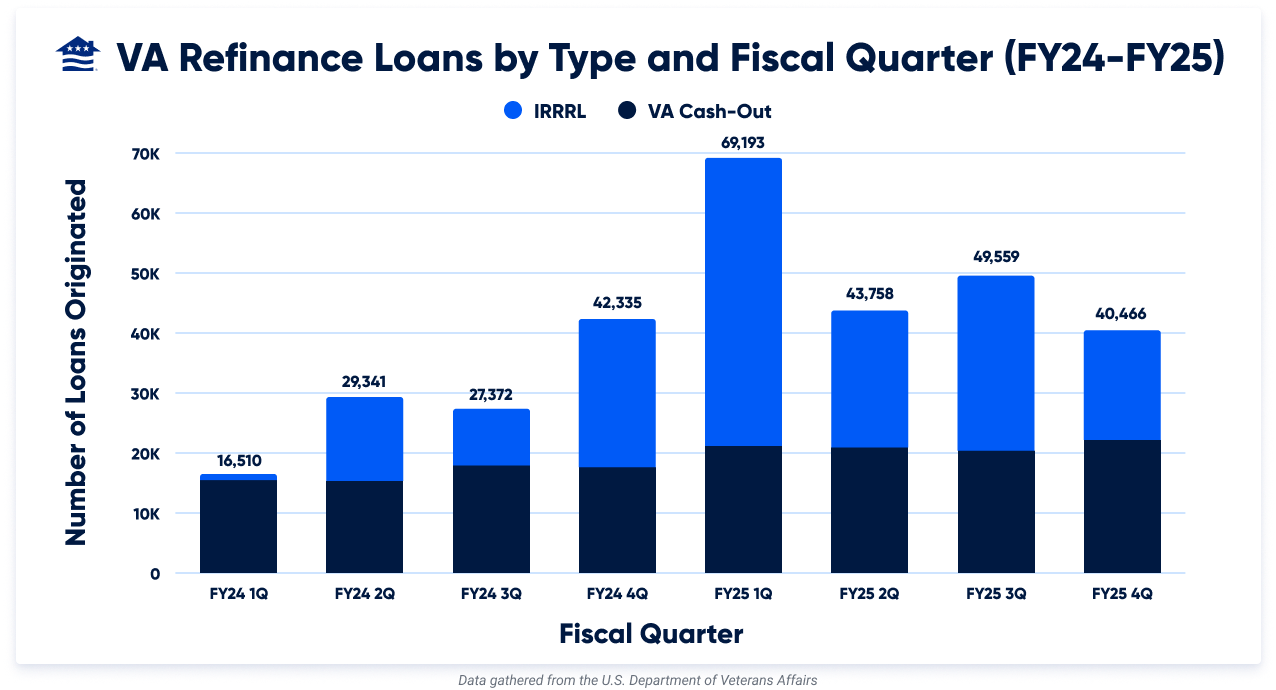

The chart below shows how Veterans have chosen between VA Streamline (IRRRL) and VA Cash-Out refinances over the 2024 and 2025 fiscal years.

VA Cash-Out refinances have trended steadily upward as more homeowners tapped their equity, but the biggest spike came from VA Streamline refinances (IRRRLs). When rates began to ease, many Veterans used IRRRLs to reduce their monthly mortgage payment, while Cash-Out refinances were more focused on accessing equity.

Answer a few questions below to speak with a specialist about refinancing your VA loan.

VA Loan Refinance Eligibility

Eligibility for a VA refinance is similar to that of a home purchase VA loan. Homeowners must still meet the VA loan service requirements.

Typically, you can qualify if you served on active duty for more than 90 consecutive days during wartime or more than 181 days of service during peacetime.

For National Guard members and Reservists, the Veteran must have served at least six years, or 90 days on Title 32 orders, 30 of which must have been consecutive.

Some surviving spouses of Veterans who died while in service or from a service-connected disability may also be eligible.

VA Refinance Guidelines

While both VA mortgage refinance options fall under the broader VA loan program, each comes with its own set of requirements. Lenders can also add their own guidelines, covering things like credit score, debt-to-income (DTI) ratio and more.

VA Streamlines were designed to be quick and easy. Many lenders won’t require a credit check, income verification or appraisal, though some may still impose their own credit score or DTI standards.

In contrast, a VA Cash-Out refinance typically involves full credit and income underwriting, similar to a VA purchase loan. Homeowners should expect to meet lender-specific requirements like minimum credit scores, DTI ratios and possibly a new appraisal.

There are also specific VA rules for each refinance option regarding how soon you can refinance. Check out VA Streamline requirements and VA Cash-Out requirements for more information.

How Soon Can You Refinance a VA Loan?

Generally, you can't refinance until 210 days after the first mortgage payment was due, and you need to have made at least six monthly on-time payments.

Seasoning guidelines for VA refinance loans can vary by lender, so ask your loan officer whether you qualify.

At Veterans United, we follow VA seasoning guidelines and typically ask for a copy of the original note or the final Closing Disclosure from the loan being refinanced, along with your most recent mortgage statement and a verification of mortgage (VOM). In some cases, we can accept alternative forms of VOM documentation.

VA Refinance Rate Trends

VA refinance rates change regularly, creating new opportunities for eligible homeowners to lower their monthly payments or tap into their home equity.

Below, you'll find the most recent trends for 30-year VA IRRRLs (Streamline refinances) and 30-year VA Cash-Out refinances:

This chart shows what the average available VA loan refinance rate was from Veterans United for each week listed. Not all consumers received this average rate and all eligibility for rates is based on individual factors including credit score.

Benefits of VA Refinancing

There are several benefits of refinancing with a VA loan. Here are some of the key advantages:

- Lower interest rates: VA refinancing often offers lower interest rates compared to conventional refinancing, which can lead to significant savings over the life of the loan.

- No private mortgage insurance (PMI): VA loans do not require PMI, even if the homeowner refinances more than 80% of their home's value. This can result in considerable monthly savings.

- Minimal upfront fees: VA Streamlines typically feature minimal costs and fees. Although the VA Funding Fee is still required for refinancing, it may be rolled into the closing costs, and some borrowers may even be exempt from paying it. Plus, the funding fee on a VA Streamline is 0.5%.

- Flexible credit requirements: VA refinancing typically has more lenient credit requirements compared to other refinancing options, making it more accessible for Veterans with less-than-perfect credit scores.

- No prepayment penalties: VA loans do not have prepayment penalties, allowing borrowers to pay off their mortgage early without any extra fees.

These benefits make VA refinancing an attractive option for those who qualify, providing financial advantages and flexibility not always found in conventional refinancing.

Should You Refinance into a VA Loan?

Refinancing into a VA loan depends on your unique financial situation. A VA refinance isn’t for everyone, but it might be the right move if you’re looking to lower your rate, access your home’s equity or make your mortgage more manageable.

Here are a few signs a VA refinance could be a great option for you:

- Rates are 0.5% to 1% lower now than when you got your current VA loan, and you want to lock in a better deal.

- You’d like to lower your monthly payment or pay off your loan sooner to save more in the long run.

- You want to use your home’s equity for renovations, repairs or other financial goals.

- You plan to stay in your home long enough to cover the cost of refinancing.

Be sure to speak directly with a VA-approved lender and run the numbers based on your personal goals, home equity and timeline.