- VA loans can be used to buy a home in another state if it will be your primary residence, with limited occupancy exceptions for active-duty service members.

- Lenders prioritize stable, ongoing income when buying out of state, often requiring a job offer or employment in the same field.

- Early planning with a VA-experienced lender and real estate agent helps reduce delays, risk and out-of-pocket costs.

Purchasing a home in a new state can be a complex process that requires careful consideration and planning. Service members and Veterans may want to use their VA benefits but wonder if it’s even possible to get a VA loan in a new state.

Can a VA Loan Be Used in Another State?

Yes, you can use your VA home loan to buy a house in another state. You must still follow VA occupancy requirements by living in the home as your primary residence and moving into the home within 60 days of closing.

VA Loan Exceptions for Moving to Another State

While VA occupancy requirements are typically heavily enforced, there are a few exceptions.

Active-duty service members with a spouse or dependent may allow the spouse and/or dependent to occupy the home while they are serving.

Service members deployed from their permanent duty station are considered to be in temporary duty status and can satisfy the requirement through intent to occupy. In this case, there is no need for a spouse or other acceptable party to satisfy occupancy.

If the home is undergoing improvements or renovations, this may also affect occupancy by possibly requiring you to wait until the construction is complete and it’s safe to inhabit.

It’s best to talk to a VA lender about your specific situation when using a VA loan in a new state to explore your options fully.

Establishing Employment

In today's digital workforce, many people can keep their current job even when moving to a new state. If you work remotely or your employer allows you to relocate while maintaining your position, this can simplify the mortgage process significantly since you'll have continuous employment history.

However, if you are changing jobs, whether by choice or by necessity, lenders will want to ensure income stability. Changing jobs before applying for a mortgage can make lenders cautious.

The lender you choose will likely want to see a job offer letter or new employment contract to ensure you will not experience a gap in employment or a significant drop in income that could affect your ability to afford a mortgage.

If you are self-employed or a contract worker, your new job should also be in the same line of work as your previous one, according to VA homebuying expert Samantha Reeves.

"Say a contractor moves to a new city and opens up a cupcake business, but the contractor doesn't have any experience making or selling cupcakes. The perceived risk is high. That's why a lender is going to want to see at least two years of experience for any new job."

Staying in the same field helps demonstrate income stability and reduces risk in the eyes of a lender.

Civilians and service members alike often do not have control over where they will live next. For civilians, that could mean following a job opportunity even if it is across the country. Military members facing a PCS move typically have a narrower range of choices when it comes to location.

Securing employment is one of the biggest requirements for buying a house in another state with a VA loan. A lender will view you as a higher risk if you do not have stable and reliable income to pay your mortgage. Once you have established new employment, you can narrow in on a location and begin selecting a lender. Reading about other borrowers’ experiences can help you find a lender that fits your situation.

Answer a few questions below to speak with a specialist about what your military service has earned you.

How to Buy a Home in a New State With a VA Loan

Using your VA home loan benefit in a new state is no easy task. There may be several obstacles, so it’s in your best interest to create a plan. Below, we break down the process and include some tips to ease your transition.

1. Choose a Lender

Finding the right mortgage lender can significantly impact your homebuying experience. While rates and fees are important, the best lender for you will also understand your unique situation and help guide you through the process with confidence.

Tips for choosing a lender:

- Look for VA loan expertise. If you’re using your VA home loan benefit, choose a lender who specializes in VA loans. They’ll understand the program’s requirements and can help you get the most from your benefits.

- Location isn’t everything. Most lenders operate online or nationwide, so you don’t need to pick one in your new city or state. Focus on reputation and service rather than proximity.

- Compare rates and fees. Even small differences in interest rates or closing costs can add up. Get quotes from multiple lenders to find the best overall value.

- Ask about communication and timelines. Choose a lender that’s responsive, transparent and keeps you informed throughout the process.

2. Getting Preapproved

After choosing a lender, your next step is getting preapproved for a mortgage. Preapproval gives you a clear picture of how much you can afford and shows sellers that you’re a serious buyer.

During preapproval, your lender will review your income, credit and debts to estimate how much you can borrow. It’s a step that helps you set realistic expectations before you start shopping and can make your offer stand out once you find the right home.

3. Find a Real Estate Agent

If you aren't yet familiar with the area you're about to move to, it may be best to enlist the help of a professional to find your new home. Ask your lender to recommend a real estate agent – one who has experience with out-of-state sales, if possible.

You can also look online for reviews and recommendations. Either way, it's important to find a real estate agent who knows the area and has experience helping buyers who are purchasing a home out of state.

If you haven't already, you'll also need to list your current home with a real estate agent in your area. While there's no way to predict how long the sale will take, it's a good idea to start receiving offers for your current home before you start making offers on a new one. You don't want to get stuck with two mortgages, so timing is key.

Let's say you start your new job on June 1. Your current house should be on the market in January, according to Greg Chaplain, a member of the Veterans United Realty Network. That will leave 60 to 90 days for you to get offers on your current home before you begin narrowing down potential new houses in March or April.

4. Choose a Specific Region

When buying a house out of state, it helps to be clear about your preferences. You might know whether you want a traditional or modern style, or if you prefer an urban or rural setting. A knowledgeable real estate agent can take these preferences and guide you toward neighborhoods that fit your lifestyle.

It's not always as simple as picking whatever's near the military base. Ask your agent to give you city or county police activity maps, government-published school information or tools that show typical commute times. Using this information can help you narrow down your search and find an area that fits your needs.

You'll have to be extra specific when giving the real estate agent a list of preferences for your new home. Since you can't be physically present for the entire home search, the list will act as a guide for the real estate agent as he or she walks through any potential prospects for you.

"We'll have a lot of conversations upfront. I'll ask some basic questions to determine your criteria and then comb through properties that meet your criteria the closest. It's like peeling back the layers on an onion. We'll peel back the layers on a fine amount of properties – 8, 10, 12, 15 – until we see what's right for your family. Let's say I send you half a dozen properties, and you say, 'I really like this one.' I'll go check it out for you and get you on the phone to walk you through it with me."

5. Make a Trip to the New State

As you near the end of your new home search, it's crucial to travel to see the property (or properties) you and your real estate agent have selected. Even the most experienced and trusted real estate agents can't possibly convey every little detail, so you'll want to see for yourself before you purchase a property.

If you’re unable to travel before closing, some buyers choose to rely on virtual tours or video walkthroughs to get a closer look at the property. While it’s not for everyone, it can be a helpful option if an in-person visit isn’t possible before closing day.

Make the trip one or two months before you're set to move or start a new job. At that point, you should have a buyer under your belt for your current home or at least be in a position to sell soon and be ready to make an offer on a new house during the trip.

6. Close on Your New Home

Once you’ve found the right home, it’s time to move toward closing. If you’re also selling your current home, timing is important.

Ideally, you’ll close on your sale before purchasing the new property to avoid carrying two mortgages at once. Work closely with your lender and real estate agent to coordinate both transactions and keep the process moving smoothly.

If you’ve used your VA loan benefit before, keep in mind that your VA entitlement may still be tied to your existing home until that loan is paid off or the property is sold. In some cases, you may have enough remaining entitlement to purchase another home, but your lender will help determine your specific eligibility.

7. Move to Your New Home

If all goes as planned during the trip, you'll be ready to start moving once you return.

The move itself, which once paled in comparison to the sell-and-buy transactions, can now seem just as stressful. While you might be able to move by yourself for a simple move up the street or to the next city over, it may be best to enlist the help of professional movers when moving to a different state.

If you can, start planning for the move at least two months in advance, generally around the time you make the trip to your new city. Begin by sifting through your possessions, selling or donating everything you no longer use. The less you have to move, the less it'll cost to move.

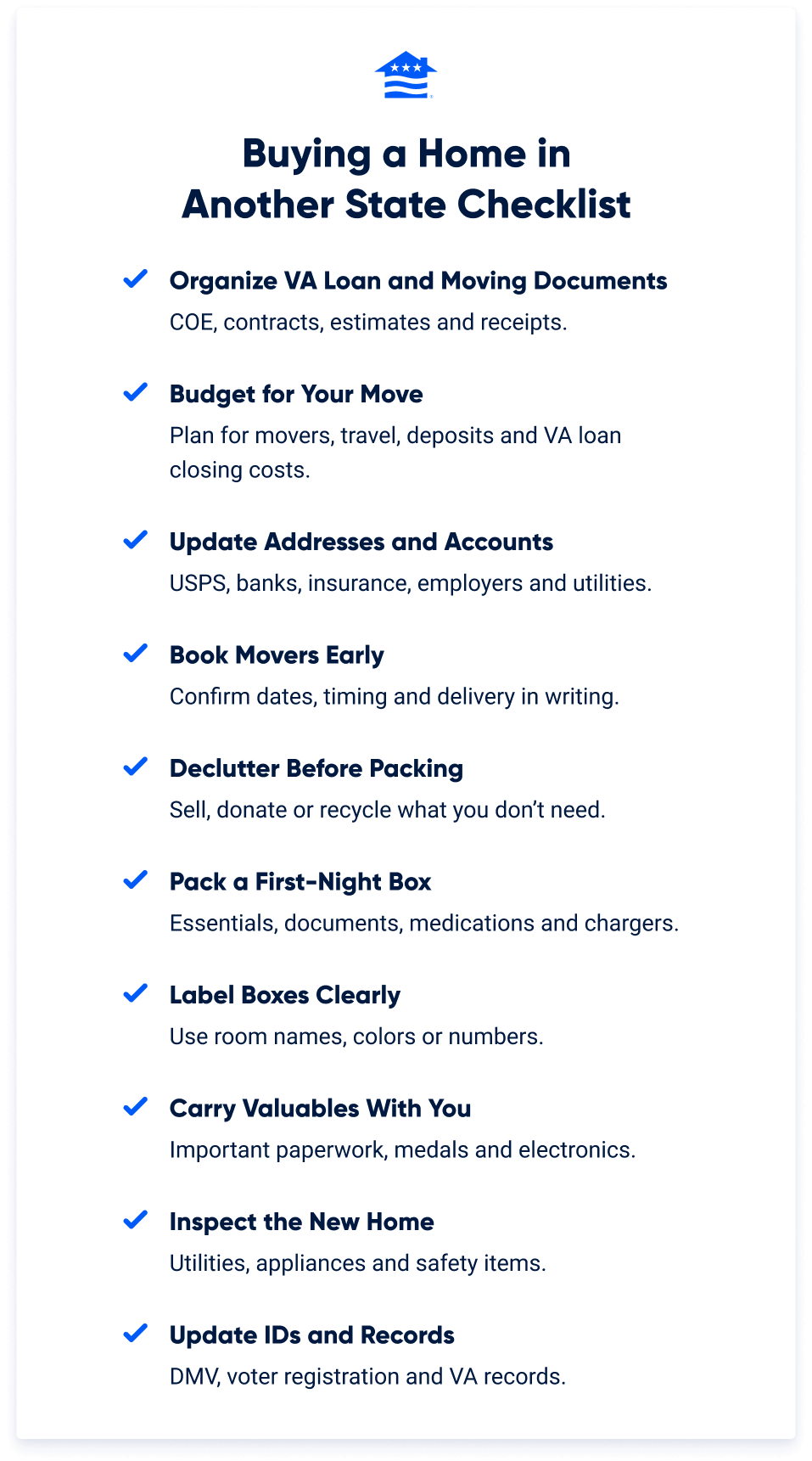

It's also important to stay organized amid the chaos. Here’s a moving checklist you can use as a reference to stay organized before, during and after your move out of state:

Buying a house in another state with a VA loan can feel overwhelming, but the right lender and real estate agent make it possible. If you’re ready to explore your options, connect with a Veterans United VA loan expert today to see how much you can save.

How We Maintain Content Accuracy

Our mortgage experts continuously track industry trends, regulatory changes, and market conditions to keep our information accurate and relevant. We update our articles whenever new insights or updates become available to help you make informed homebuying and selling decisions.

Current Version

Mar 26, 2026

Written ByChris Birk

Reviewed ByTara Dometrorch

Minimal article updates for clarity and to include a graphic checklist. Content reviewed and fact check by team lead underwriter Tara Dometrorch.

Related Posts

-

What is the VA Seller Concession Rule?Seller concessions with a VA home loan can save Veteran homebuyers thousands of dollars, but cannot exceed 4% of the loan.

What is the VA Seller Concession Rule?Seller concessions with a VA home loan can save Veteran homebuyers thousands of dollars, but cannot exceed 4% of the loan. -

VA Loan Discount PointsPurchasing discount points on a VA loan can be a good investment for Veterans looking to lower their interest rate.

VA Loan Discount PointsPurchasing discount points on a VA loan can be a good investment for Veterans looking to lower their interest rate.