- VA loans usually require no down payment and no ongoing mortgage insurance, making them more affordable long-term than FHA loans.

- FHA loans may be easier to qualify for if you have a lower credit score or higher DTI.

- VA loans typically have lower interest rates and no loan limits with full entitlement.

FHA and VA loans are both popular government-backed mortgage options, but they differ significantly in eligibility, down payment requirements, mortgage insurance and long-term cost. Deciding which option is right for you comes down to your unique financial circumstances.

FHA loans, insured by the Federal Housing Administration, are accessible to the general public. In contrast, VA loans are backed by the Department of Veterans Affairs and available to Veterans, active duty service members and some surviving spouses.

Let’s take a look at how the two mortgage types compare.

FHA vs VA Loan Volume

Based on the most recent HMDA data, 906,942 FHA loans were originated in 2025 compared to almost 561,783 VA loans.

Difference Between FHA and VA Loans

Government-backed mortgages, like FHA and VA loans, are generally more affordable compared to conventional loans and offer appealing terms for first-time homebuyers, low-income borrowers and those with lower credit.

While mortgage lenders and banks do the lending, the government insures these loans, lowering the lender's risk and allowing for more flexible requirements.

Below is a table outlining the key factors to consider when comparing VA loans to FHA loans.

FHA vs VA Loans at a Glance

| Comparison Factor | FHA Loan | VA Loan |

|---|---|---|

| Eligibility | Available to the general public | Only available to active-duty service members, Veterans, members of the National Guard or Reserves and surviving spouses |

| Down Payment | At least 3.5%, but depends on credit score | None required |

| Credit Score Minimum | 500 to 579 with a minimum down payment of 10% or at least 580 with a 3.5% down payment | None set by VA, but lenders often require at least 620 |

| Interest Rates* | Slightly higher than VA | Slightly lower than FHA |

| Property Requirements | Must be primary residence and meet FHA Minimum Property Standards | Must be primary residence and meet VA Minimum Property Requirements |

| Debt-to-Income Ratio | Up to 50% | Up to 41% |

| Loan Limits | $541,287 in low-cost counties to $1,249,125 in high-cost counties | None if the borrower has full entitlement |

| Mortgage Insurance and Fees | An upfront premium and annual premium | VA Funding Fee |

| Refinancing | FHA Streamline or FHA Cash-Out refinance; mortgage insurance required | VA Streamline (IRRRL) or VA Cash-Out refinance; no mortgage insurance |

Eligibility

A major difference between FHA and VA loans is who is eligible for the loan. FHA loans are accessible to all qualified borrowers, which is particularly beneficial for first-time homebuyers or those with lower credit scores.

On the other hand, VA loans are specifically designed for military service members, Veterans and eligible surviving spouses. Eligibility criteria for VA loans are centered around service requirements, while FHA loans focus on financial and creditworthiness benchmarks.

Takeaway: If you are a Veteran or active-duty service member, VA loans are generally the better option over FHA loans.

Down Payment

FHA loans are available to the broader public and typically require a minimum down payment of 3.5% for borrowers with a credit score of 580 or higher. Those with credit scores between 500 and 579 are required to make a 10% down payment.

There’s no down payment requirement with a VA loan, meaning you don’t have to put any money down if you have your full VA entitlement. This is a major benefit of the program and enables individuals to finance 100% of the home's value.

Takeaway: For eligible borrowers, a VA loan is usually the stronger choice over an FHA loan if you don’t have enough saved for a down payment. Learn more about how to buy a home with no down payment and what it takes to qualify.

Credit Score Requirements

FHA loans typically have a minimum credit score requirement of around 580, but that can vary by lender. Borrowers with a score below this threshold may still qualify but might be required to make a larger down payment.

VA loans are more lenient in terms of credit score and don’t have a strict minimum credit score requirement. Loan approval is more dependent on the lender’s discretion. VA lenders often look at the overall credit profile rather than focusing solely on the credit score. A common benchmark is a credit score of 620, but this may vary by lender.

Takeaway: If your credit score is below 620 and you can afford a down payment, an FHA loan is probably the best bet.

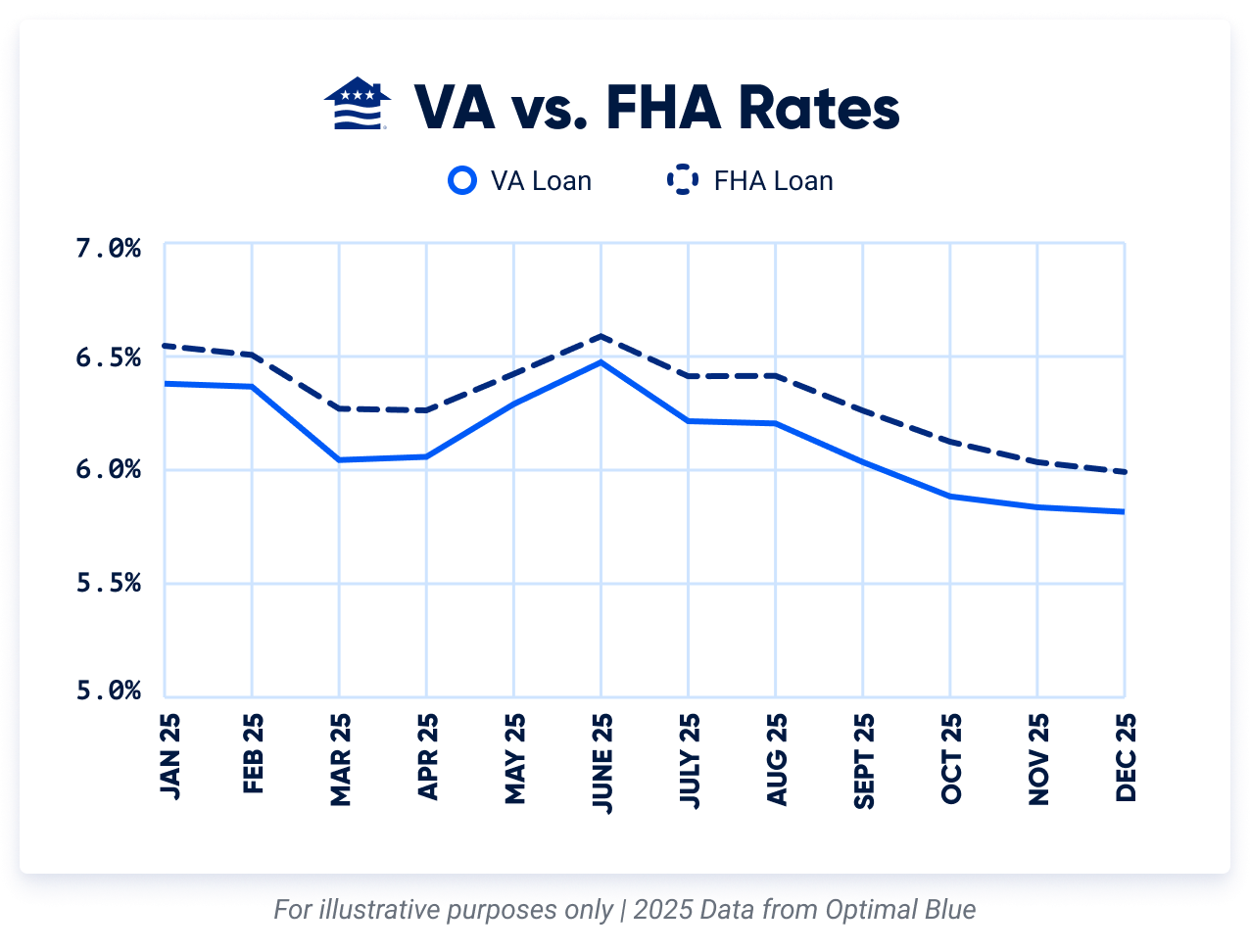

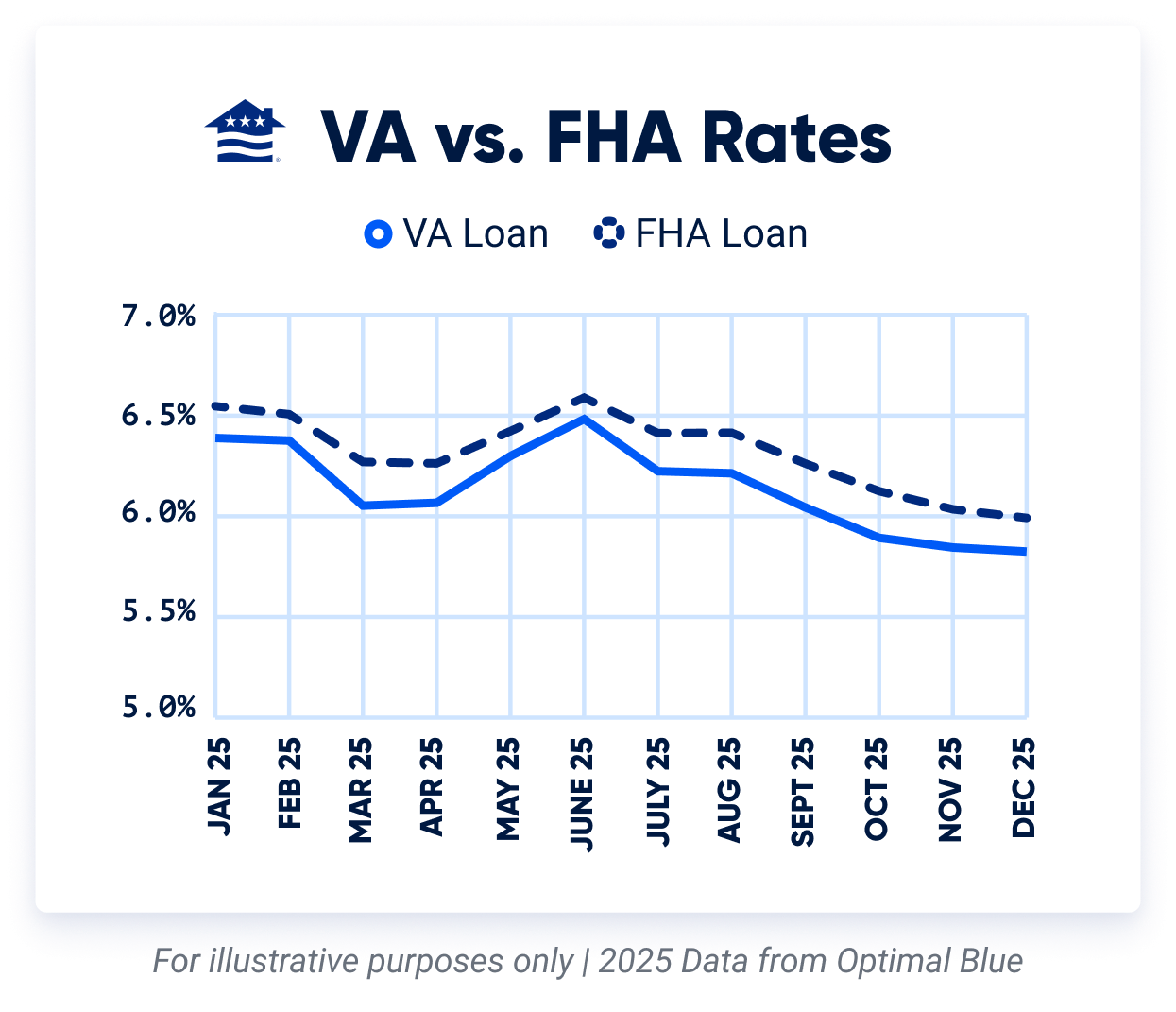

Interest Rates

Since VA and FHA loans are both government-backed, they can offer more favorable interest rates. According to Optimal Blue, VA loan rates remained about 0.19% lower on average than FHA rates in 2025. You can check current VA loan rates to see how today's numbers compare.

Let’s break down the monthly payments and total interest paid for both types of loans, assuming a loan amount of $200,000 over a 30-year period with a 0.19% difference in interest rate. Important to note: when factoring in a standard 3.5% down payment for the FHA loan, the total interest paid between the two loans is very similar, so the main difference in cost comes from the upfront down payment.

Comparing VA and FHA Loan Total Interest

| Loan Type | Interest Rate | Monthly Payment | Total Interest Paid |

|---|---|---|---|

| VA Loan | 5.825% | $1,176.69 | $223,609.14 |

| FHA Loan | 6.015% | $1,158.99 | $224,237.99 |

Takeaway: Over the last year, VA interest rates were slightly lower than FHA. However, interest rates largely depend on your financial situation. Use our VA loan calculator to estimate your monthly payments and see how a lower rate could impact your long-term costs.

Property Requirements

VA and FHA loans take a similar approach to property requirements — both programs require the home to be a primary residence and meet minimum standards for safety, structural integrity and overall condition before financing is approved.

FHA loans require an appraisal and have specific property standards covering the home's structural integrity and key systems, including electrical, heating and plumbing. These standards are designed to ensure the property's safety and security for the borrower.

VA loans have comparable requirements, including an appraisal to assess the home's value and condition. Where VA loans differ slightly is in their specific Minimum Property Requirements (MPRs), which are tailored to ensure the home is safe, sanitary and structurally sound for Veterans and their families.

Takeaway: Both FHA and VA loans require a home appraisal to meet property requirements and must be used for the borrower’s primary residence.

Debt-to-Income Ratio

The debt-to-income (DTI) ratio represents the proportion of your gross monthly earnings that is used to pay off debts, including the mortgage payment.

The maximum DTI ratio for FHA loans is generally 50%. However, there may be exceptions that allow higher DTI with compensating factors.

The VA doesn’t set a maximum DTI ratio. However, borrowers exceeding a ratio of 41% are subject to an in-depth assessment to ensure their residual income is sufficient to manage living costs after making mortgage or other debt payments.

Takeaway: If you have a DTI ratio greater than 41%, you may have an easier time getting approved for an FHA loan.

Answer a few questions below to speak with a specialist about what your military service has earned you.

Loan Limits

FHA loan limits are capped and vary depending on the county and state where the property is located. These limits are set to ensure that the program caters to low to moderate-income homebuyers. FHA loan limits are slightly more constricting, with a common maximum borrowing amount of $541,287 for single-family homes.

VA loans do not have a maximum loan limit if you have your full VA entitlement. However, limits may still apply to those who have previously used the VA loan benefit or have diminished VA entitlement.

Takeaway: When it comes to loan limits, VA loans usually offer more flexibility because borrowers with full VA entitlement can borrow without a loan limit cap, while FHA loans have maximums that can restrict your purchasing power.

Mortgage Insurance and Fees

FHA loans come with two mortgage insurance charges – an upfront insurance premium and a yearly mortgage insurance premium (MIP) based on the remaining loan balance. The one-time upfront charge on FHA loans is 1.75% of the loan amount and is added to your loan balance.

The annual MIP can only be canceled once your mortgage is paid in full, unless you made a down payment of at least 10%. In that case, the MIP will be canceled after 11 years.

The VA Funding Fee varies from 1.25% to 3.3% of the loan amount, depending on the down payment amount and previous VA loan use. This fee can be paid upfront or rolled into the total loan amount. Some VA loan applicants are exempt from paying the funding fee entirely, including Veterans receiving compensation for a service-connected disability, surviving spouses eligible for a VA loan, Purple Heart recipients and Veterans who would receive disability compensation but are on active duty.

As of 2026, the funding fee is also now tax-deductible, much like mortgage interest. Eligible Veterans and service members can claim it by itemizing deductions and reporting the fee as an upfront mortgage insurance premium. Since the deduction can vary based on your filing situation, working with a tax professional is the best way to make sure you're claiming it correctly.

Takeaway: When evaluating FHA vs VA loans, it's important to calculate the total costs over the life of the loan, including upfront costs and annual mortgage insurance premiums.

Refinancing

Both VA and FHA loans offer refinancing options, but VA borrowers generally have more flexibility with choices that can lower their rate, eliminate mortgage insurance or tap into home equity.

VA borrowers can choose between two VA loan refinancing options: the VA Streamline refinance (IRRRL), which is designed to lower your monthly payment with minimal paperwork and often no appraisal required, and the VA Cash-Out refinance, which allows eligible homeowners to tap into their home's equity for things like home improvements or paying off debt. Closing costs can typically be rolled into the loan amount, making it a low out-of-pocket option for many Veterans.

FHA borrowers have access to a streamline refinance to lower their rate, as well as a separate cash-out refinance option, but both come with ongoing mortgage insurance requirements that VA loans don't require. Veterans who currently have an FHA loan can use the VA Cash-Out refinance to switch into a VA loan, potentially eliminating their monthly mortgage insurance premium in the process.

Takeaway: VA borrowers have two dedicated refinance options, and eligible Veterans with an FHA loan can refinance into a VA loan to eliminate ongoing mortgage insurance costs.

Is FHA or VA Loan Better?

For eligible Veterans, VA loans are generally the better option due to no down payment, no monthly mortgage insurance and lower average interest rates. But, FHA loans may be a stronger fit for borrowers with lower credit scores or higher debt-to-income ratios.

A VA loan is likely the best choice if you want to maximize your buying power, as there is no down payment requirement and no loan limits for borrowers with full entitlement. Although there is a one-time VA Funding Fee, you may qualify for an exemption based on your service-connected disability status.

An FHA loan may make more sense if your credit score falls below the typical VA lender minimum of 620, or if you have not served in the military and are therefore ineligible for a VA loan.

No matter your homebuying goals, Veterans United is here to help. Connect with a home loan expert to get a complete comparison for your unique homebuying journey.

How We Maintain Content Accuracy

Our mortgage experts continuously track industry trends, regulatory changes, and market conditions to keep our information accurate and relevant. We update our articles whenever new insights or updates become available to help you make informed homebuying and selling decisions.

Current Version

Jun 12, 2026

Written ByChris Birk

Reviewed ByDon Wilson

Updated data and graphics to reflect full 2025 calendar year and added additional information on refinancing. Content fact checked and reviewed by underwriter Don Wilson.

Dec 12, 2025

Written ByChris Birk

Updated FHA loan limits for 2026.

Jun 20, 2025

Written ByChris Birk

Updated figures to reflect 2025 data.

Apr 3, 2025

Written ByChris Birk

Updated Home Mortgage Disclosure Act (HMDA) origination figures for FHA and VA loans with data updated in 2025.

Dec 13, 2024

Written ByChris Birk

Updated FHA loan limits to 2025 numbers: $524,225 in low-cost areas and $1,209,750 in high-cost areas.

Veterans United often cites authoritative third-party sources to provide context, verify claims, and ensure accuracy in our content. Our commitment to delivering clear, factual, and unbiased information guides every piece we publish. Learn more about our editorial standards and how we work to serve Veterans and military families with trust and transparency.

- Home Mortgage Disclosure Act, 2025. For 2024, about 825,000 FHA loans were originated compared to almost 490,000 VA loans.

- Optimal Blue Mortgage Market Indices. VA loan rates remained .19 percent lower on average than FHA in 2025.

- U.S. Department of Housing and Urban Development. Streamline refinance options for FHA-insured mortgage.

Related Posts

-

How to Make an Offer on a HouseOnce you’ve found the right home, you need to know how to put together a purchase offer. Learn tips for putting an offer on a house with a VA loan.

How to Make an Offer on a HouseOnce you’ve found the right home, you need to know how to put together a purchase offer. Learn tips for putting an offer on a house with a VA loan. -

A Guide to Joint VA LoansUnderstand the eligibility criteria, process and advantages of joint VA loans and how they can be a valuable resource for Veterans or service members.

A Guide to Joint VA LoansUnderstand the eligibility criteria, process and advantages of joint VA loans and how they can be a valuable resource for Veterans or service members.