- VA loans cannot be used to purchase land alone, as the purchase must happen simultaneously with new home construction.

- Veterans have three paths to use VA benefits for land: finance land and construction together, use separate financing to build and then refinance into a VA loan or build on land you already own.

- Most lenders don't offer VA land and construction loans, and those that do may require a down payment, so a construction-to-VA refinance is often the more practical route.

Between money-saving benefits, such as 0% down and no mortgage insurance, Veterans and service members wishing to purchase a home will be hard-pressed to find a better option than the VA loan.

But what if you don't wish to purchase a previously occupied home? Can the VA loan help you buy land and build a custom, more personalized home?

Can You Buy Land With a VA Loan?

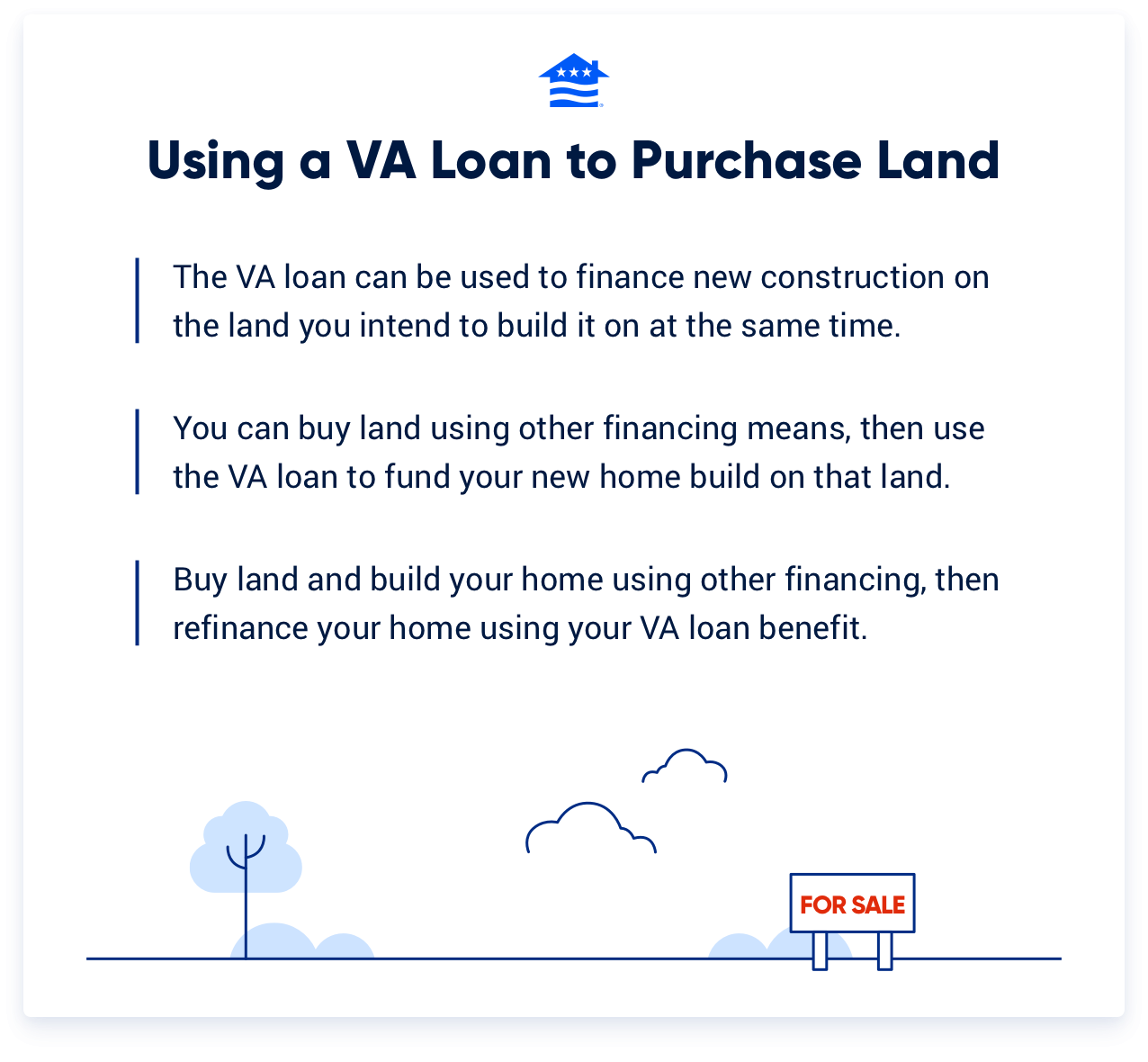

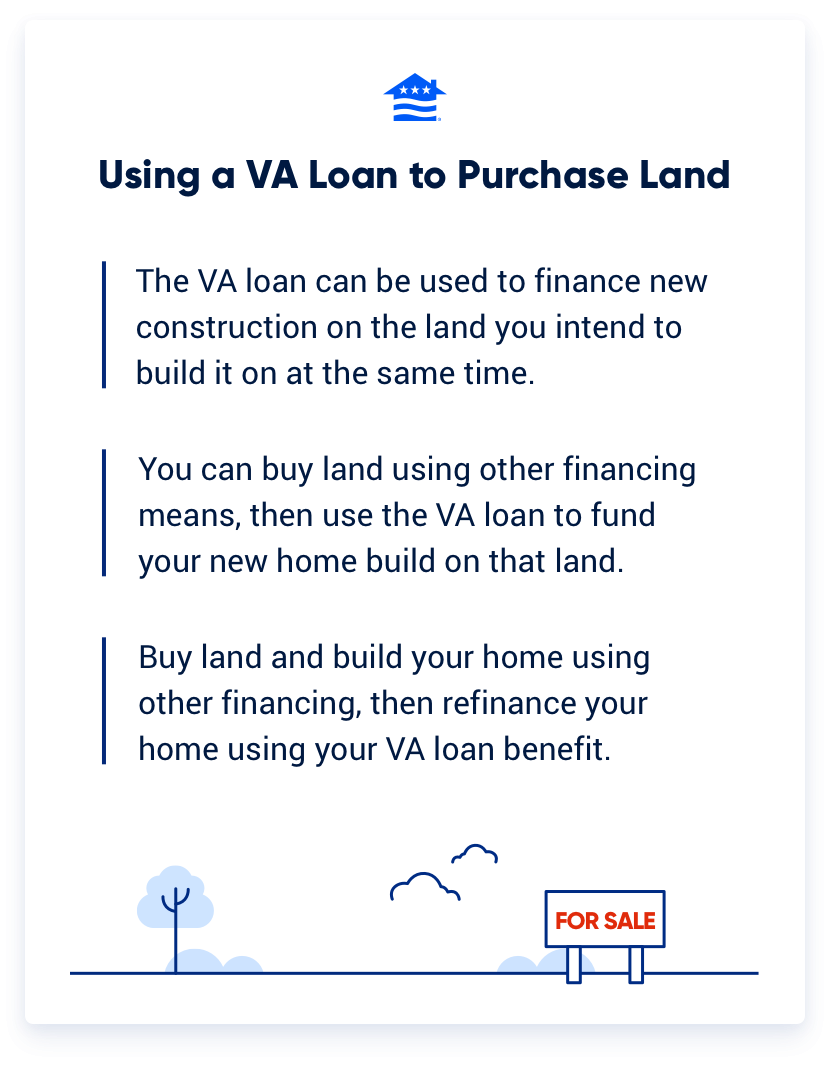

Yes, you can buy land with a VA loan, but only if you're building a home on it at the same time. You can't use a VA loan to purchase land by itself, even if you intend to build a home later.

How to Buy Land With a VA Loan

It sounds confusing, but the gist is simple: Buying only land? A VA loan won't work. Buying land and building on it right away? The VA will allow it.

There are generally three options if you're looking to buy land with your VA loan benefits:

- Finance Land and Construction Together: Use a VA loan to finance both the construction of your proposed home and the land you intend to build it on simultaneously.

- VA Construction-Only Loan: Buy land using some other means of financing. Then use your VA loan benefit to fund the construction of your home.

- Construction-to-VA Refinance: Buy land and construct your home using some other means of financing - typically a short-term construction loan. Then, once finalized, refinance the construction loan into a VA loan.

If you already own land or inherited a parcel of it, you're free to use a VA loan to build upon it. And if you used a different loan type to purchase the land initially, you may be able to VA refinance once the home construction is complete.

If you’re a Veteran who wants to buy a newly built home with a VA loan, there are also options worth exploring. VA loans can be used for homes that are already built or nearly complete, and the process tends to go smoothest when the home is close to finished. Just keep in mind that the home must meet VA Minimum Property Requirements and serve as your primary residence.

Does Veterans United Do Land Loans?

Veterans United, like most VA loan lenders, does not offer land loans or new construction loans. However, we do regularly work with Veterans interested in these kinds of loans. Veterans who find a builder or local lender to construct their home can often refinance their home into a VA loan after closing.

Get connected with an experienced VA lender to discuss your construction loan options.

Rules for Buying Land and Constructing a Property

As with all VA loans, there are some particular requirements you'll need to meet if you plan to buy land and construct a property using your benefits.

Here are the big ones:

- The property you construct can be no more than four units. Each unit must have its own water, sewage, gas and electricity connections, and you must live in one of the units as your primary residence.

- The property must be affixed to a permanent foundation.

- The property must meet the VA's Minimum Property Requirements and must comply with all federal and local building standards.

- The land can't be located in a flood or noise zone (airstrip, highway, railroad tracks, etc.).

- The land can't be located near a landfill, dump or hazardous material facility.

- The land can't be vulnerable to landslides, earthquakes or other geologic instabilities.

Of course, you'll also need a valid Certificate of Eligibility, and your builder must be licensed and insured. While VA Builder IDs are no longer required, builders still need to meet VA and lender standards. Learn more about the ins and outs of VA construction loans here.

VA Loans for Land and Construction Aren't Common

While the VA technically allows it, most lenders don't offer VA loans for purchasing land and construction. These types of loans are generally riskier, and if you do find a lender that offers one, there may be additional down payment requirements to offset the risk.

You can avoid this by using a construction loan or other financing product to fund your land purchase and home construction, then refinance into a VA loan once the home is built. In this scenario, you'd then be eligible for the traditional zero-down-payment VA loan.

The Bottom Line on VA Land Loan Requirements

Buying land with a VA loan is possible, but it comes with strict requirements and isn't always the most straightforward path to homeownership.

If you're a Veteran considering a land loan, connecting with a knowledgeable VA lender early can help you understand your options and find the financing path that makes the most sense for your situation.

Answer a few questions below to speak with a specialist about what your military service has earned you.

How We Maintain Content Accuracy

Our mortgage experts continuously track industry trends, regulatory changes, and market conditions to keep our information accurate and relevant. We update our articles whenever new insights or updates become available to help you make informed homebuying and selling decisions.

Current Version

Jun 26, 2026

Written ByChris Birk

Reviewed ByDon Wilson

Minor copy updates to improve readability. Content fact checked and reviewed by underwriter Don Wilson.

Feb 3, 2025

Written ByChris Birk

Reviewed ByDon Wilson

Content fact checked and reviewed by underwriter Don Wilson.

Related Posts

-

VA Renovation Loans for Rehab & Home ImprovementVA rehab and renovation loans are the VA's answer to an aging housing market in the United States. Here we dive into this unique loan type and the potential downsides accompanying them.

VA Renovation Loans for Rehab & Home ImprovementVA rehab and renovation loans are the VA's answer to an aging housing market in the United States. Here we dive into this unique loan type and the potential downsides accompanying them. -

Pros and Cons of VA LoansAs with any mortgage option, VA loans have pros and cons that you should be aware of before making a final decision. So let's take a closer look.

Pros and Cons of VA LoansAs with any mortgage option, VA loans have pros and cons that you should be aware of before making a final decision. So let's take a closer look.