Taking a leave of absence—whether planned or unexpected—can introduce unique challenges, particularly when you're in the process of applying for a mortgage. Extended time away from work often brings questions about income, stability, and how it might impact your ability to qualify for a loan.

This article explores how different types of leave, such as maternity or paternity leave, medical leave, or unpaid leave, may affect your VA mortgage application and provides actionable steps to navigate the process.

Family and Medical Leave Act (FMLA)

The Family and Medical Leave Act (FMLA) protects eligible employees from losing their jobs during certain types of leave, such as maternity leave or medical leave. If your paid leave is covered under FMLA and your income remains the same, your mortgage application may proceed as planned.

However, FMLA doesn’t guarantee pay—just job protection—so if your income decreases or stops during your leave, that may complicate your mortgage process. To confirm how your situation aligns with FMLA, check your employer's policies or consult with an employment attorney.

For more information on FMLA, visit Family and Medical Leave Act.

How VA Loans Are Affected by Leaves of Absence

When applying for a VA loan, lenders require proof of stable, ongoing income to ensure you can reliably make mortgage payments. If your income changes due to a leave of absence, lenders evaluate your financial stability based on several factors:

- Is your leave paid or unpaid?

- How long will your leave last?

- Will your income resume at the same level upon returning to work?

The VA loan program has unique advantages, such as flexibility around debt-to-income (DTI) ratios, but income stability is non-negotiable. Working with a VA mortgage specialist can help clarify how your leave impacts eligibility.

Reduced Pay During Absence

If your income is reduced during leave, you may still qualify for a VA loan, but you’ll need to provide documentation, including:

- Pay stubs reflecting reduced pay.

- A letter of explanation outlining the reason for your leave.

- A verification of employment letter from your employer detailing your pay, leave status, and return-to-work date.

In some cases, qualifying on reduced income is possible if your debt-to-income ratio remains manageable. However, be prepared for lenders to scrutinize your financial situation more closely.

Frequently Asked Questions (FAQs)

Can I apply for a mortgage while on maternity or paternity leave?

Yes, but your eligibility depends on whether your income remains stable during your leave. Lenders may require additional documentation to verify your pay and employment status.

What if I am self-employed and take a leave of absence?

Self-employed individuals may face greater challenges, as lenders typically require proof of consistent income over two years. If you anticipate reduced income, consult a mortgage specialist for guidance.

Does taking leave affect my credit score?

No, taking leave doesn’t directly impact your credit score. However, missing payments on bills or loans during unpaid leave can negatively affect your credit.

State-by-State Leave Laws

In addition to federal FMLA protections, some states have their own leave laws that may provide additional benefits. For example:

- California: Offers up to 8 weeks of Paid Family Leave (PFL) with partial income replacement.

- New York: Provides paid family leave for up to 12 weeks.

Check your state’s labor department for specific benefits that may apply to you. These can influence your financial situation and eligibility for a mortgage during leave.

The Bottom Line

Taking a leave of absence doesn’t have to derail your dream of homeownership. With careful planning, open communication, and the right guidance, you can still achieve your goals. It's always important to notify your VA mortgage specialist if you have advance notice of any type of leave that will reduce or stop your pay completely prior to closing on a home. By notifying your VA mortgage specialist and being proactive you can determine your home purchasing timeline and how this leave will extend it, if at all.

If you would like to discuss your specific situation further, please feel free to email me at samantha@vu.com!

How We Maintain Content Accuracy

Our mortgage experts continuously track industry trends, regulatory changes, and market conditions to keep our information accurate and relevant. We update our articles whenever new insights or updates become available to help you make informed homebuying and selling decisions.

Current Version

Dec 10, 2024

Written BySamantha Reeves

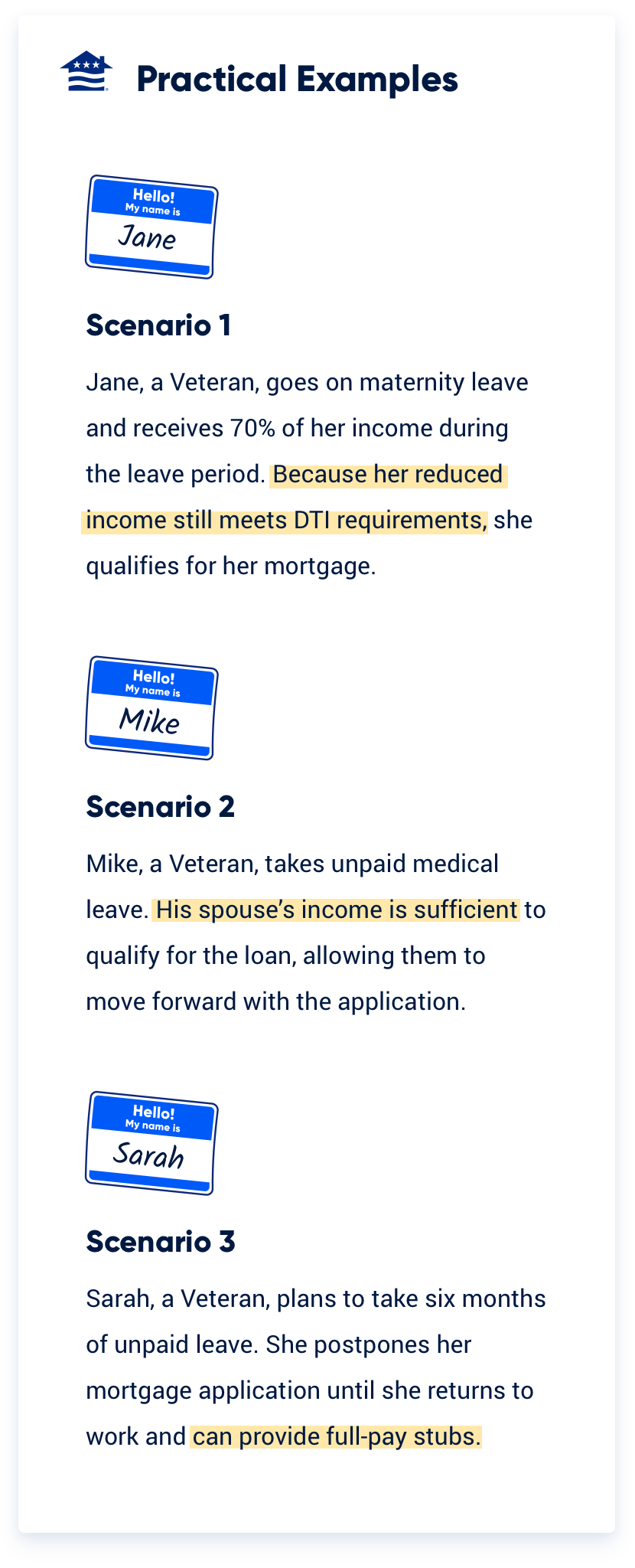

Revised this article to enhance its performance by adding more in-depth, reader-focused content. Given that the original was published in 2013, it required a modern update to align with current standards and expectations. Added a FAQ section and a practical examples graphic to improve usability and reader engagement.

Related Posts

-

What is the VA Seller Concession Rule?Seller concessions with a VA home loan can save Veteran homebuyers thousands of dollars, but cannot exceed 4% of the loan.

What is the VA Seller Concession Rule?Seller concessions with a VA home loan can save Veteran homebuyers thousands of dollars, but cannot exceed 4% of the loan. -

VA Loan Discount PointsPurchasing discount points on a VA loan can be a good investment for Veterans looking to lower their interest rate.

VA Loan Discount PointsPurchasing discount points on a VA loan can be a good investment for Veterans looking to lower their interest rate.